Jana Small Finance Bank’s plans for expansion took an unexpected hit as the Reserve Bank of India (RBI) recently returned its application for a universal bank license. The move comes just as Jana SFB was eyeing a shift to broader banking services, hoping to join the league of major commercial banks in India. This development delays the bank’s aspirations to access new business opportunities, reduce funding costs, and expand its product portfolio.

Jana Small Finance Bank Faces Setback

Jana Small Finance Bank’s experience shows the challenging journey SFBs must undertake to attain universal bank status in India. The RBI’s decision sets high benchmarks for governance and operational excellence, and Jana’s proactive stance positions it well for future opportunities once compliance gaps are closed.

RBI Returns Jana Application

The RBI’s action was not a total rejection but a “return” of the proposal, meaning the bank may resubmit its application after meeting the necessary criteria. While the central bank did not specify all deficiencies publicly, sources suggest that gaps in regulatory compliance, profitability record, and asset quality led to the decision. Jana SFB management has stated they will soon meet with RBI officials to clarify requirements, rectify shortcomings, and reapply, treating this as a temporary pause rather than a final denial.

Reasons Behind the Jana SFB Setback

The key reason for this regulatory development is Jana SFB’s current inability to fully meet all the eligibility criteria set under RBI’s guidelines for small finance banks transitioning to universal status. These criteria include being listed, having a scheduled bank status, maintaining a net worth of at least ₹1,000 crore, and sustaining profits with low non-performing assets (NPAs) for two years.

Business Impact and Current Operations of Jana Small Finance Bank

This regulatory pause has delayed the bank’s move to potentially lower its borrowing costs and broaden its offerings, especially in co-lending activities- one of the privileges of a universal bank. However, Jana SFB continues normal operations as before, serving 12 million customers with a wide range of banking products.

Sector Context: A Pattern of Heightened Scrutiny

The RBI’s thorough review of Jana SFB’s proposal reflects the regulator’s growing caution. Only a handful of SFBs, such as AU Small Finance Bank, have received in-principle approvals recently, while others like Ujjivan SFB are also awaiting decisions. This underscores RBI’s focus on strong compliance, asset quality, and sustainable growth before granting universal bank licenses.

Jana SFB’s Response and Future Outlook

The management has expressed confidence in addressing the feedback, strengthening the bank’s operations, and reapplying as soon as eligible. Jana SFB sees the situation as a temporary pause, not a denial, and remains committed to its regulatory obligations and target of long-term, nation-wide growth.

National Safe Motherhood Day 2026, Theme...

National Safe Motherhood Day 2026, Theme...

CNP Nashik Recruitment 2026, Apply Onlin...

CNP Nashik Recruitment 2026, Apply Onlin...

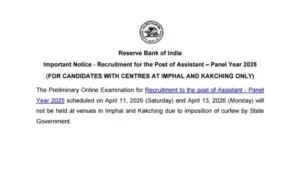

RBI Assistant Prelims Exam 2026 Postpone...

RBI Assistant Prelims Exam 2026 Postpone...