The Reserve Bank of India (RBI) has introduced a fresh draft framework in 2026 aimed at reforming how loan recovery is handled across banks and financial institutions. These proposed rules are designed to ensure fairness, transparency, and accountability in the recovery process while safeguarding borrower rights.

Why RBI Introduced New Draft Recovery Rules in 2026

With the rapid expansion of retail lending, digital loans, and unsecured credit products, loan recovery practices have also evolved. However, concerns related to borrower harassment, misuse of data, and aggressive collection tactics prompted the need for a structured and uniform framework.

The RBI’s 2026 draft rules aim to:

- Standardize recovery practices across all regulated entities

- Protect borrowers from unethical or coercive conduct

- Strengthen grievance redressal systems

- Increase transparency in engagement of recovery agents

Key Highlights of RBI Draft Loan Recovery Rules 2026

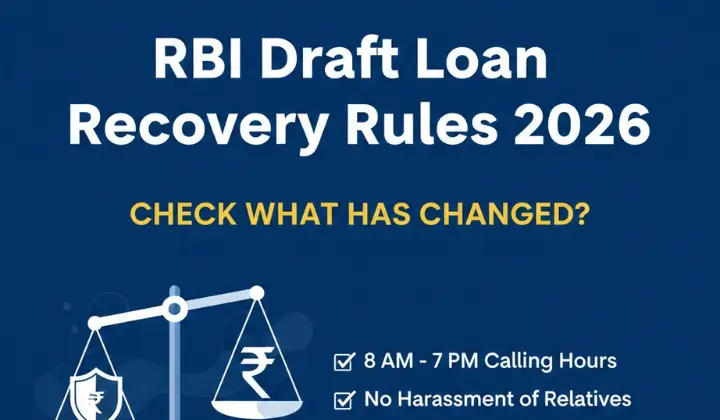

1. Clear Definition of Unacceptable Recovery Practices

Any form of intimidation, humiliation, or mental harassment is strictly barred under the proposed framework. The draft explicitly prohibits:

- Threatening or abusive communication

- Repeated or excessive calls

- Public shaming or contacting relatives/social circles unnecessarily

- Misleading statements regarding legal consequences

2. Fixed Communication Hours

Recovery agents and bank representatives can contact borrowers only during prescribed hours typically between 8:00 AM and 7:00 PM unless specifically agreed otherwise.

This prevents late-night calls or inappropriate timing that may cause distress.

3. Mandatory Disclosure of Recovery Agents

Institutions are also required to maintain a publicly accessible list of authorized recovery agents. Banks and NBFCs must:

- Inform borrowers in writing before assigning a recovery agent

- Provide full details including name and contact credentials

- Update borrowers if there is a change in agent

4. Board-Approved Recovery Policy

This ensures internal accountability and professional standards. Each regulated entity must have:

- A board-approved recovery policy

- A clear Code of Conduct for recovery staff and third-party agents

- Proper training and certification for agents

5. Call Recording and Monitoring

All recovery-related communications must be recorded and properly documented. Banks are required to maintain call logs and interaction records for audit and compliance purposes.

6. Stronger Grievance Redressal Mechanism

If a borrower has filed a complaint:

- The account should not be immediately referred to a recovery agent

- The grievance must be addressed first

7. Due Process Before Asset Possession

Taking possession of secured assets cannot be the first recovery step. Banks must:

- Follow proper legal procedures

- Ensure prior communication and fair notice

- Respect borrower rights throughout the process

Who Will Be Covered Under These Draft Rules?

The proposed guidelines apply to:

- Scheduled Commercial Banks

- Small Finance Banks

- Regional Rural Banks

- Cooperative Banks

- NBFCs

- Housing Finance Companies

What Makes the 2026 Draft Different?

Compared to earlier general fair-practice guidelines, the 2026 draft:

- Clearly defines “harassment”

- Prescribes fixed communication hours

- Mandates documentation and call recording

- Links grievance handling directly to recovery actions

- Requires stronger board-level oversight

What This Means for Borrowers

- Protection from coercive tactics

- Clear information about who is contacting them

- Limited and regulated communication hours

- Better complaint resolution support

What This Means for Banks & NBFCs

- Higher compliance responsibility

- Greater monitoring of third-party agents

- Mandatory training and documentation

- Increased accountability for recovery conduct

A Random YouTube Class That Led Nishita ...

A Random YouTube Class That Led Nishita ...

Adda247 Classroom Experience Now Availab...

Adda247 Classroom Experience Now Availab...

Upcoming Bank Clerk Exams 2026, Salary, ...

Upcoming Bank Clerk Exams 2026, Salary, ...