Under the Employee’s Provident Fund and miscellaneous provisions act, 1952 two schemes were framed: Employee’s Provident Fund (EPF) and Employee Pension Scheme (EPS). EPF and EPS are administered by the Central board of trustees consisting of both central and state government representatives, employers, and employees. What is the difference between EPF and EPS? We will be answering this question with a detailed explanation so keep reading.

What is an Employee Provident Fund (EPF)?

The Employee Provident fund is a scheme that promotes saving towards an individual‘s retirement. It is a fixed income retirement benefits scheme that is available for all employees in the corporate sector. In this scheme, both the employer and the employee of an establishment contribute which gets accumulated until the end of the individual’s working period.

What is the Employee Pension Scheme (EPS)?

The employee pension scheme is a scheme that pays pensions to the employees. The scheme is especially available to employees who are the member of EPFO and also to those who have contributed to the EPS account. The contribution in EPS is from the employer’s side. The employer’s contribution in EPS is 8.33% of the basic salary of an employee. The employee pension scheme is activated and received after the age of 58 years.

Difference Between EPF and EPS

EPF and EPS or different schemes and have different benefits. To understand the difference between EPF and EPS candidates must read the table mentioned below thoroughly:

| Element | EPF | EPS |

| Employee’s contribution | 12% of basic salary and dearness allowance | Nil |

| Employer’s contribution | 3.67% of basic salary and dearness allowance paid to the employee | 8.33% of the basic salary and dearness allowance paid to the employee |

| Eligible employees | All | Employees whose salary + dearness allowance is up to Rs.15,000 |

| Interest on investment | EPF is calculated every month and paid at the end of the FY.

The interest rates of EPF are fixed and reviewed by the government regularly. |

No interest is paid on the EPS account |

| Maximum contribution | The contribution is 12% on salary. | The Contribution is limited to 8.33% on salary up to Rs.15,000, i.e. Rs. 1250 |

| Tax | Interest received on EPF account is exempt

But if the contribution is more than Rs.2.5 lakh in any year. Then tax is payable on excess amounts. If the balance amount in EPF is withdrawn before 5 years, then TDS @10% is deducted. No tax on principal amount redemption |

Pension and lump-sum amounts both are taxable when received. |

| Withdrawal of funds | After 58 years of age or if unemployed for a continuous period of 60 days or more | Pension is received after 58 years of age. |

FAQs: Difference Between EPF and EPS

Q. What is the full form of EPS?

Ans: The Full form of EPS is Employee Pension Scheme.

Q. What is the full form of EPF?

Ans: The Full form of EPF is Employee Provident Fund.

Q. What is the Employee’s contribution to EPF?

Ans: 12% of basic salary and dearness allowance.

![Symbiosis Entrance Test [SET] Test Series 2027 | Test Series by Adda247](https://storeimages.adda247.com/image111759237214.png)

![Symbiosis Entrance Test [SET] Test Series 2026 | Test Series by Careers Adda](https://storeimages.adda247.com/image1sybiosis1764929799.png)

SBI PO Salary 2026, Check New CTC, Perks...

SBI PO Salary 2026, Check New CTC, Perks...

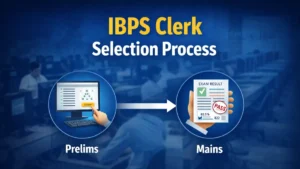

IBPS Clerk Selection Process 2026, Check...

IBPS Clerk Selection Process 2026, Check...

IBPS Clerk Notification 2026 (Short) Out...

IBPS Clerk Notification 2026 (Short) Out...