The banking industry plays an important role in financial stability and economic growth. This sector is not immune to various risks that can potentially threaten its operations, profitability, and overall stability. Major risks in the Banking Sector is a topic that holds significant importance for upcoming banking and government examinations such as RBI Grade B, SEBI, NABARD, SBI PO etc. Understanding these risks not only helps candidates in written exams but is also crucial for the interview.

By thoroughly understanding the information presented in this piece, readers can gain valuable awareness and knowledge about the subject matter, which will undoubtedly prove beneficial in the General Awareness section of various banking and government recruitment examinations. The article aims to equip readers with a comprehensive understanding of the risks inherent in banking operations, encompassing the fundamental concepts and precise definitions of each risk type.

What Are Major Risks in Banking?

Let’s first understand the concept of major risks in the banking sector in layman’s language. In the banking context, risk represents the uncertainty surrounding future earnings and potential outcomes in the event of failure. Risks can stem from inadvertent staff errors or malicious intent, resulting in the depreciation of asset values and ultimately diminishing the intrinsic worth of the bank.

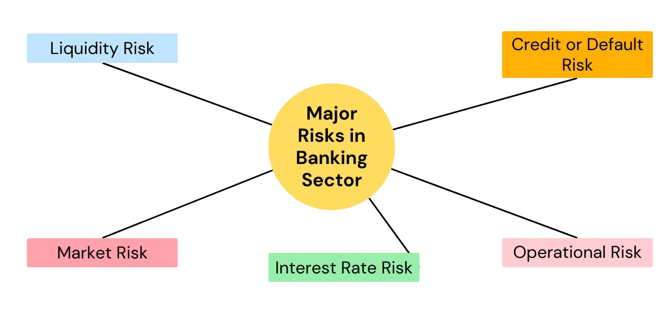

In other words, Risks in the banking sector refer to the potential for unfavorable deviations from expected outcomes, arising from various uncertainties inherent to banking activities. These risks represent the possibility of losses or adverse impacts due to the divergence between actual and anticipated returns or results. Some of the major risks in the banking sector encountered in Indian banking are credit risk, market risk, operational risk, liquidity risk, business risk, reputational risk, and systemic risk.

For Example: The Punjab National Bank (PNB) faced a fraud amounting to Rs. 11,400 crores. The risk category impacted by this incident includes credit risk, operational risk, and reputational damage.

Types of Risks in the Banking Sector

The banking sector is exposed to various types of risks, which can have significant impacts on its operations, financial stability, and overall performance. Understanding and effectively managing these risks is crucial for maintaining a sound and resilient banking system. Here’s an overview of major risks in the banking sector, along with detailed explanations:

Liquidity Risk

Banks face liquidity risk when they finance long-term assets using short-term liabilities, exposing those liabilities to rollover or refinancing challenges. This risk entails the potential for an institution to be incapable of fulfilling its maturing obligations, or to do so only by borrowing funds at exorbitant rates or by selling assets at significantly reduced prices. The liquidity risk in banks manifests in different dimensions –

- Funding Liquidity Risk: Funding liquidity risk refers to the difficulty in securing funds to fulfill cash flow commitments. This issue occurs when there is a need to cover net outflows caused by unexpected withdrawals or the non-renewal of both wholesale and retail deposits.

- Time Risk: Time risk occurs due to the necessity to make up for the lack of anticipated fund inflows, which happens when performing assets become non-performing assets.

- Call Risk: Call risk emerges from the materialization of contingent liabilities. It can also occur if a bank is unable to seize profitable business opportunities when they arise.

Interest Rate Risk

Interest Rate Risk (IRR) occurs when fluctuations in interest rates influence an institution’s Net Interest Margin or Market Value of Equity (MVE). IRR can be considered from two perspectives: its effect on the bank’s earnings or its impact on the economic value of the bank’s assets, liabilities, and Off-Balance Sheet (OBS) positions. The following are the types of Interest Rate Risk –

- Gap or Mismatch Risk: Gap or mismatch risk stems from having assets, liabilities, and Off-Balance Sheet items with varying principal amounts, maturity dates, or re-pricing dates. This situation exposes the institution to unforeseen fluctuations in market interest rates.

- Basis Risk: Basis risk occurs when the interest rates of various assets, liabilities, and off-balance sheet items may fluctuate to varying extents.

- Embedded Options Risk: Substantial shifts in market interest rates pose a risk to banks’ profitability as they prompt early repayment of cash credit/demand loans, term loans, and the exercise of call/put options on bonds/debentures, or premature withdrawal of term deposits before their scheduled maturities.

- Reinvested Risk: Reinvestment risk emerges from the uncertainty surrounding the interest rate at which future cash flows may be reinvested.

- Net Interest Position Risk: Net Interest Position Risk occurs when market interest rates decrease, and banks hold more earning assets than paying liabilities. In such cases, banks witness a decrease in Net Interest Income (NII) as market interest rates decline, and NII rises when interest rates increase.

Market Risk

Market Risk refers to the potential for unfavorable changes in the mark-to-market value of the trading portfolio, caused by market fluctuations, while the transactions are being liquidated. This risk arises from adverse movements in the prices of interest rate instruments, equities, commodities, and currencies, either in their level or volatility.

- Forex Risk: Forex risk entails the possibility of a bank incurring losses due to unfavorable fluctuations in exchange rates while holding an open position, whether spot, forward, or a combination of both, in a specific foreign currency.

- Market Liquidity Risk: Market liquidity risk occurs when a bank faces difficulty in executing a significant transaction for a specific instrument at or close to the prevailing market price.

Operational Risk

As per the Basel Committee for Banking Supervision, operational risk is characterized as the potential for financial loss stemming from insufficient or malfunctioning internal processes, personnel, and systems, as well as external occurrences. Consequently, operational losses primarily stem from three areas of exposure: individuals, procedures, and technological systems.

Transaction Risk

It stems from either fraudulent activity, ineffective business procedures, or the incapacity to sustain business operations and handle information proficiently.

Compliance Risk

Compliance risk refers to the potential for a bank to face legal penalties, financial setbacks, or damage to its reputation due to its inability to adhere to relevant laws, regulations, codes of conduct, and standards of ethical practice. It is also known as integrity risk because a bank’s reputation is closely associated with its commitment to principles of integrity and equitable behaviour.

Other Risks in the Banking Sector

Strategic Risk

Strategic risk emerges from unfavorable business choices, inadequate execution of decisions, or failure to adapt to shifts within the industry. It hinges on how well an organization aligns its strategic objectives with its business strategies, allocates resources, and executes its plans effectively.

Reputation Risk

Reputation risk stems from unfavorable public perception, potentially leading to legal action, financial repercussions, or a reduction in the institution’s customer base.

Risk Management Practices In India

Risk management, as described by knowledge theorists, encompasses the management of uncertainty, risk, equivocality, and error. Uncertainty, characterized by an inability to predict outcomes even randomly, stems from insufficient information. As information gathering progresses, uncertainty transitions into risk, where outcomes can be estimated. With increasing knowledge about markets and potential outcomes, risk management offers strategies for mitigating risk. Equivocality arises from conflicting interpretations and a resulting lack of clear judgment. Given the dynamic nature of the market, banks must remain vigilant about the alignment of regulatory frameworks within the country, shifts in international accounting standards, and notably, changes in clients’ business practices. Thus, it is imperative to adhere to specific risk management guidelines recommended by both the RBI and BIS.

Role of RBI in Risk Management in Banks

The Reserve Bank of India employs the CAMELS rating system to assess the financial stability of banks. This model comprises six key components: Capital Adequacy, Asset Quality, Management, Earnings Quality, Liquidity, and Sensitivity to Market Risk.

In 1988, the Basel Committee on Banking Supervision, a part of the Bank for International Settlements (BIS), suggested the utilization of capital adequacy, asset quality, management quality, earnings, and liquidity (CAMEL) as benchmarks for evaluating a financial institution. In CAMELS framework Rating 1 is best whereas rating 5 is worst. CAMELS stands for-

C-Capital Adequacy: Evaluates the bank’s capital sufficiency via analysis of capital trends, risk management capabilities, economic conditions, loan quality, growth strategies, and other relevant factors.

A-Asset Quality: Evaluate the quality of loans extended by the bank.

M-Management: Evaluates the institution’s ability to manage financial pressure effectively.

E-Earnings: Assesses the institution’s capacity to generate suitable returns for expansion, maintaining competitiveness, and bolstering capital.

L-Liquidity: Evaluate a company’s liquidity by considering the availability of short-term assets that can be swiftly converted into cash.

S-Sensitivity: Addresses the impact of specific risk exposures on institutions by overseeing the management of credit concentrations.

Importance of Risk Management in the Banking Sector

The core objective of risk management practices within the banking sector is to boost the value proposition for stakeholders by maximizing profitability and optimally allocating capital resources. This approach ensures the long-term financial stability and solvency of the banking institution. By striking a balance between prudent risk-taking and effective risk mitigation strategies, banks can enhance their ability to generate sustainable returns while maintaining a robust financial footing, ultimately benefiting all parties with vested interests in the organization’s success.

IBPS PO PET Call Letter 2026 Out, Downlo...

IBPS PO PET Call Letter 2026 Out, Downlo...

NABARD Development Assistant LPT Result ...

NABARD Development Assistant LPT Result ...

Bank of India Credit Officer Admit Card ...

Bank of India Credit Officer Admit Card ...