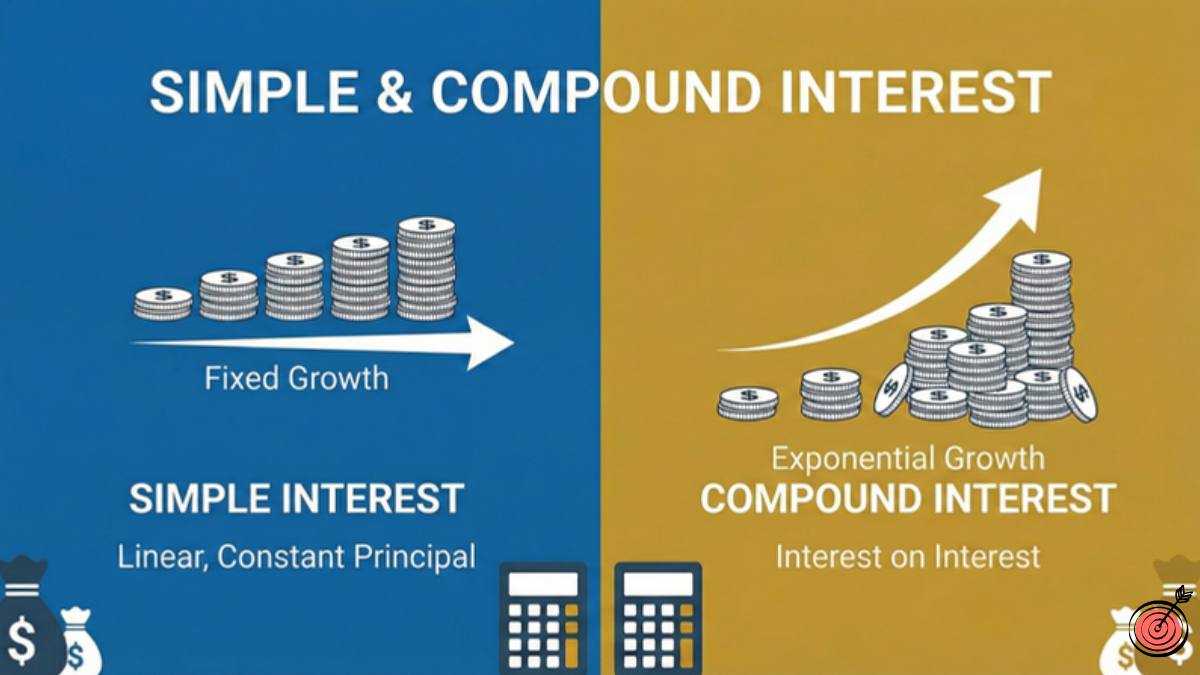

Understanding interest is one of the most important concepts in banking, finance, and competitive exams. Whether you’re preparing for bank exams or simply trying to manage money better, knowing how Simple Interest (SI) and Compound Interest (CI) work can help you make smarter financial decisions.

What is Simple Interest?

Simple Interest is the interest calculated only on the original principal amount, making it straightforward and predictable. The interest earned remains the same every year because it does not compound. It is commonly used in short-term loans, education loans, and basic financial transactions. Overall, SI is simple to compute and easy to understand.

Formula:

SI = (P × R × T) / 100

Where:

-

P = Principal

-

R = Rate of Interest

-

T = Time (in years)

Example:

If you invest ₹10,000 at 10% for 2 years:

SI = (10000 × 10 × 2) / 100 = ₹2,000

This means the total amount after 2 years = ₹12,000.

What is Compound Interest?

Formula:

Amount = P (1 + R/100)^T

CI = Amount – P

Example:

Invest ₹10,000 at 10% for 2 years:

Amount = 10000 (1 + 10/100)² = 10000 × 1.21 = ₹12,100

CI = 12,100 – 10,000 = ₹2,100

Because interest gets added every year, CI is higher than SI.

Why Does CI Grow Faster?

Because each year’s interest gets added to the principal, the amount on which interest is calculated keeps increasing. This effect is called compounding, and it helps your money grow faster over time.

Where Are SI & CI Used?

Simple Interest

-

Short-term loans

-

Car loans

-

Agriculture loans

-

Quick manual calculations in exams

Compound Interest

-

Fixed deposits (FDs)

-

Recurring deposits (RDs)

-

Long-term investments

-

Credit cards

-

Loans with compounding periods

Quick Tips to Solve SI & CI Questions in Exams

- Always identify P, R, and T clearly.

- For CI questions, check compounding frequency (yearly, half-yearly, quarterly).

- Use formula shortcuts when possible.

- Compare SI and CI carefully. CI is always greater except for a 1-year duration.

Linear and Circular Seating Arrangement ...

Linear and Circular Seating Arrangement ...

Detailed Comparision Between RBI Assista...

Detailed Comparision Between RBI Assista...

NBFC Full Form

NBFC Full Form